What is the 95% mortgage guarantee scheme?

In April 2021 the Government announced a scheme to support a new generation in buying a home. The introduction meant that the availability of 95% loan-to-value (LTV) mortgages was made much easier.

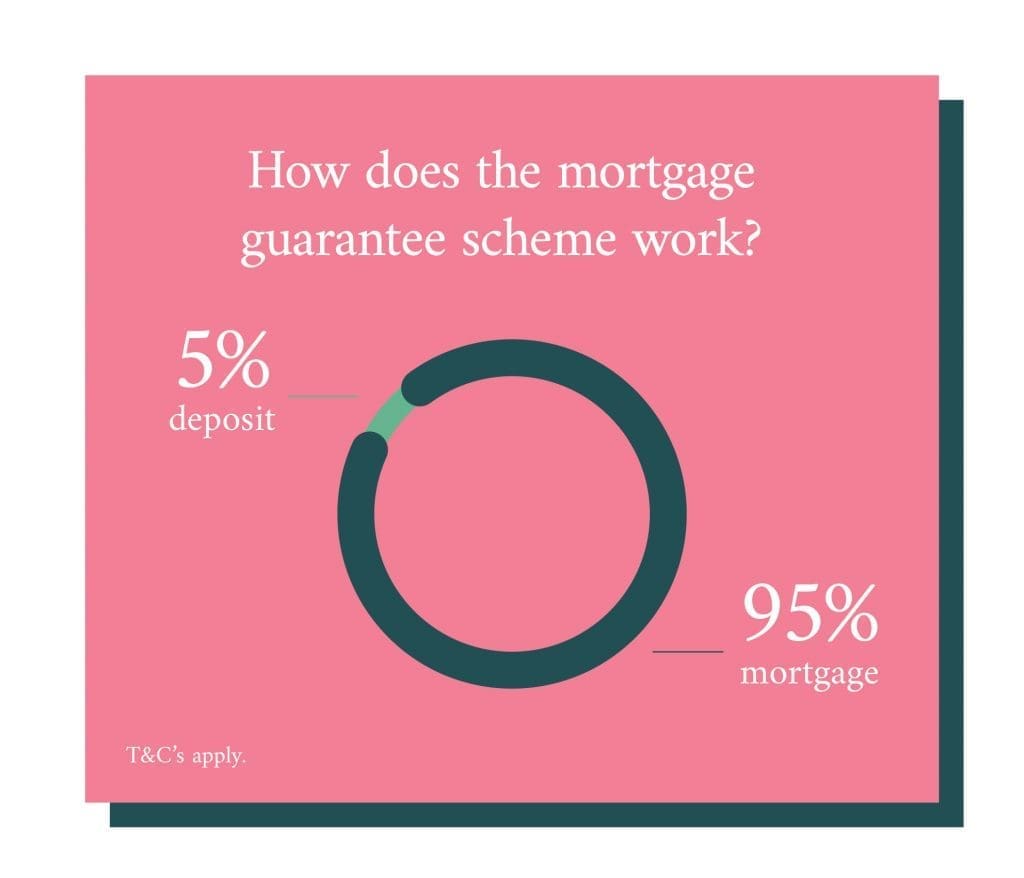

Essentially, lenders can choose to be compensated for part of their losses in the event of a repossession. In turn, the borrower will only need to provide a 5% deposit on the property, which makes lending much less risky.

The scheme was initially scheduled to finish at the end of 2023. However, it has since been announced that it will be extended until 30th June 2025. This government mortgage scheme has been backed by initial funding of £150 million. From April 2021 to June 2023 the scheme helped a little over 39,000 people complete a mortgage.

Do you qualify?

No credit checks & only takes minutes!

The scheme similar to the Government’s previous Help to Buy shared equity scheme, although there are some key differences between the two. Firstly, the Help to Buy scheme is designed for first-time buyers and the equity loan is paid to the developer.

With the Help to Buy scheme the applicant would arrange a mortgage with a personal 5% deposit in the same way. However, the 20% equity loan would be paid on practical completion. On completion of the build, the loan is paid to the lender, and in turn, the loan-to-value is reduced to 75% of the build cost.

Why has the Government introduced the scheme?

In 2020 the Government looked to provide some impetus to the housing market by putting in place a stamp duty tax holiday, giving savings of up to £15,000 to some would-be homebuyers. Whilst this had its desired effect, many lenders started to restrict the availability of their mortgage ranges and one sector to suffer the most the higher loan-to-value mortgage.

Nearly all lenders withdrew these from the market in entirety and although we have seen a good number of 90% LTV options return, 95% loans still remain scarce.

The 95% LTV mortgage guarantee scheme therefore has been introduced to encourage lenders to re-enter this arena.

Mortgage Guarantee Scheme explained?

The perceived risk by lenders when offering 95% mortgages has seen many simply withdraw from this market. The scheme will therefore provide a guarantee to the lender, by the Government, for any loan offered at 95% loan-to-value.

It’s important to understand that this guarantee is provided for the lender and not you as the intended borrower. It will also mean that lenders won’t take a more lenient view of your finances when underwriting your application. Affordability will still remain an important aspect of their assessment, as will your credit history.

In line with the additional risk that lenders will place on 95% loan-to-value mortgages, expect this to be reflected in the interest rates they offer. These will likely be higher than their schemes for 90% mortgages.

Sadly, not all lenders will engage with the new scheme, therefore do expect there to be a reduced number of options available.

Fill out our quick and easy Mortgage Affordability calculator below. We only require a few details to see how much you may be able to borrow.

NO CREDIT CHECKS!

Mortgage guarantee scheme lenders

Although certain lenders choose not to use the scheme, there’s still a range that do. From our experience we have worked with the following lenders on mortgage guarantee applications:

If you’re unsure about your lending options, why not reach out today. Our expert advisers will be able to run over your situation and advise you on the most suitable option.

Mortgage guarantee scheme eligibility

As with any government housing scheme, there will be certain criteria that need to be fulfilled. Fortunately, the 95% LTV mortgage guarantee scheme has been introduced with these kept to a minimum.

It’s available to first-time buyers and home-movers can use the scheme for the purchase of new build properties and those on resale. The only restriction of note is the maximum purchase price of £600,000.

How to apply for the Governments mortgage guarantee scheme?

There is no separate application process for a customer to be approved for the “scheme”. It is simply part of the mortgage application when you apply for a 95% mortgage with a participating lender. Therefore, this makes the whole process fairly straightforward.

We understand that with numerous schemes available to provide assistance to many looking to purchase their home, it can be confusing as to which you may be eligible for and indeed which may suit you best.

The 95% LTV Mortgage Guarantee Scheme officially starts with effect from April 2021 and here at The Mortgage Centres, all our advisers are fully trained and in a position to assist you. Why not make us your next step towards purchasing your new home and contact us today for your free initial consultation.

"*" indicates required fields